Making Money With Real Estate

All the secrets distilled into one article

Do you want a proper property analysis done? Do you want aid in the calculations of your real estate adventure? Reach out to me; contact@futurefunds.nl or send me a private message.

Figure 1, Funda

Having explored the macroeconomic factors shaping the Dutch real estate market in our previous article, we now turn to the practical mechanics of real estate investment. The persistent housing shortage and favorable interest rate trends create an appealing environment for property investors, but how do you actually do this?

In this article, we'll examine a concrete example using a real property listed on Funda, with potential for student housing. The home's layout could potentially accommodate five students, with its location near a university enhancing its investment appeal.

We'll show how understanding real estate market dynamics at the macro level can be applied to generate returns at the property level. As interest rates continue their downward trend and housing shortages persist, these investment fundamentals become essential for anyone looking to understand how to make money with real estate.

Understanding and Pairing the Assets and Liabilities

The success of any real estate investment ultimately comes down to a fundamental equation: do your inflows exceed your outflows? This balance between assets and liabilities determines whether a property will generate wealth or drain resources.

Every property operates with two financial sides: income streams (assets) and expenses (liabilities). The art of successful investing lies in structuring these elements to create positive cash flow and long-term appreciation.

On the asset side, rent serves as your primary revenue source. Student housing offers a particular advantage here, with multiple rental streams from several tenants creating a diversified income base. This diversity provides stability even when individual rooms become temporarily vacant. The cornerstone of maintaining high occupancy is location, properties near universities or city centers consistently experience higher demand among students, significantly reducing vacancy risks.

Your liability side presents a bit more complexity. Mortgage payments typically represent your largest expense, as we explored in comparing linear and annuity structures previously. Property taxes constitute an unavoidable annual cost that varies by location and assessment. Maintenance expenses fluctuate year to year, ranging from minor repairs to significant investments in aging systems or structural issues.

What distinguishes real estate from other investments is the initial setup period required. Beyond the purchase itself, you'll need to invest in renovations to optimize the space for your target market. In this case, creating functional, comfortable student accommodations.

This setup period actually presents a strategic opportunity. If you possess handyman skills or connections with reliable contractors, you can dramatically impact your returns through cost-effective renovations, potentially transforming an ordinary property into a high-performing asset. With thoughtful management of both your income streams and expense obligations, you create a sustainable wealth-building vehicle capable of delivering returns for decades.

Before purchasing the property, also check the regulations in the municipality, whether it is permitted to convert a home into student units at this specific location. These days law is a big part of real estate investing and should not be overlooked.

Real Life Example, Maastricht Tongersestraat

As this article is about making money, let's examine a real-life example that could be executable if you have sufficient time and capital. The property we'll analyze can be seen in Figure 1, the white house with the brown door.

When you look at the current Funda listing photos, you might be taken aback. This highlights the first reality of real estate that many "gurus" conveniently gloss over: this isn't free money. The truth is that successful real estate investing involves adding value to properties by remodeling them to serve a better purpose in society. This process is neither simple nor easy, it requires significant capital investment and considerable hard work.

I've specifically chosen this property as our example because of its minimal state. This "blank canvas" offers numerous possibilities for transformation, making it ideal for demonstrating the real process of creating value in real estate investment. Next to this, Maastricht is still an investor friendly environment for developing student houses, as permits are still given out here.

Figure 2, Funda

As you can see in Figure 2 it can be possible to make 5 middle big student rooms in this house. The set up would probably be 1 room on the ground floor and a kitchen with living area, 2 on the first floor and 2 at the second floor. Potentially we could transform the basement into a bathroom to obtain a complete student house. Before we continue philosophizing on how we can best remodel this house to accommodate these students it is important to see if we can even make this financially work.

The Math

Now that we understand the potential of converting this property into student housing, let's analyze whether this investment makes financial sense. The numbers need to work before we commit to any renovation plans.

Based on market research for student housing in Maastricht, we can reasonably expect to charge approximately €550 per month per student (with students paying their own utilities). With five rooms available for rent, this would generate a total monthly income of €2,750, or €33,000 annually. This rental income will likely increase with inflation, which we'll model at a conservative 2% annual rate to match the Consumer Price Index (CPI).

For this investment, we'll need to borrow €500,000 through a mortgage. Given current market conditions, we can secure a 30-year annuity mortgage at a fixed 4% interest rate, resulting in annual mortgage payments of €28,645.

Figure 3

As shown in Figure 3, these mortgage payments will constitute the largest portion of our expenses over the 30-year period. Additional expenses include property tax (based on the WOZ value) estimated at €1,500 per year, which will also increase at approximately 2% annually. Since we'll be completely renovating the property at purchase, we can reasonably assume no significant maintenance costs for the first 5 years. After this period, we'll allocate 3% of rental income for annual maintenance – a reasonable estimate for a well-renovated property where tenants are contractually responsible for keeping the place in good condition. These combined expenses are visualized in the stacked bar chart above.

The total purchase and renovation plan involves a property purchase price of €350,000, with our mortgage amount of €500,000 and our own investment of €100,000, leaving us with €250,000 available for renovation. This significant renovation budget allows us to transform the property into an optimized student housing facility.

When we subtract our expenses from the rental income, we get the net cash flow shown below.

Figure 4

Considering our initial investment of €100,000, these cash flows represent a strong return that increases steadily over time. Furthermore, after 30 years, the mortgage will be fully paid off, and all rental income (minus expenses) becomes pure profit.

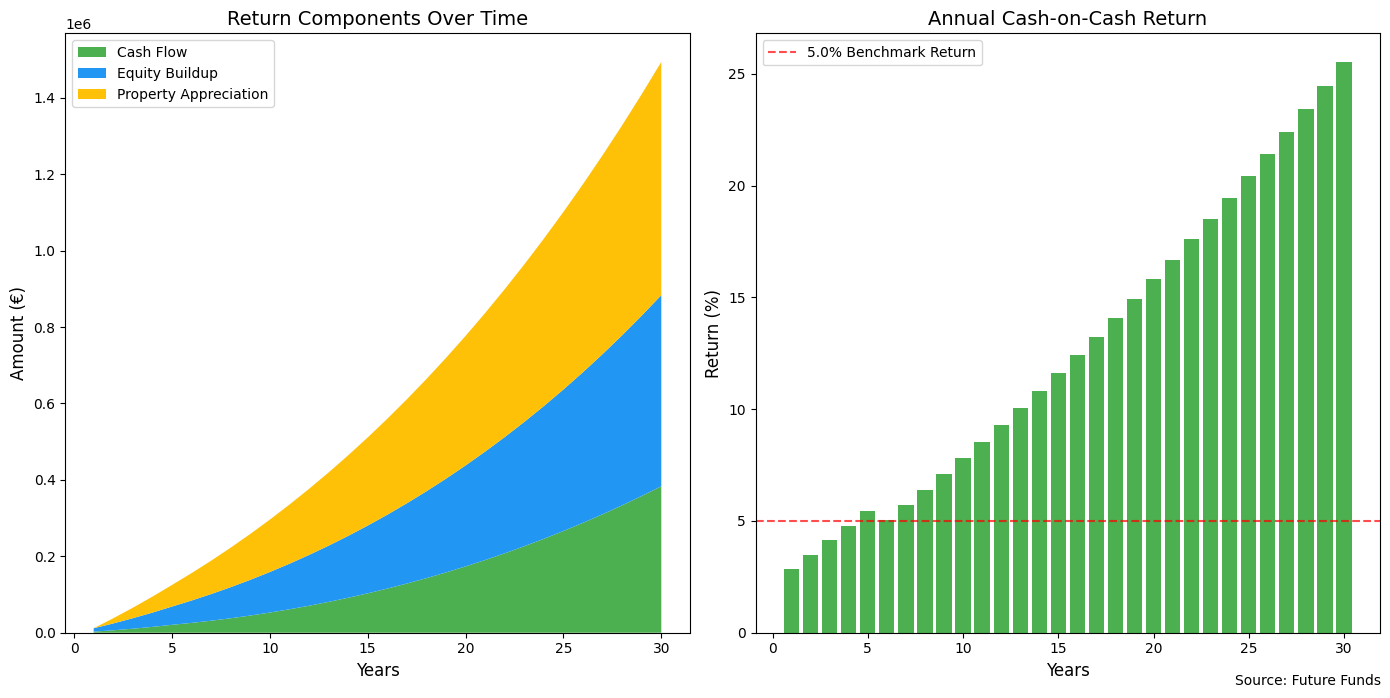

Figure 5

As illustrated in Figure 5, real estate investment provides multiple streams of returns: regular cash flow from rental income, equity buildup as you pay down the mortgage, and property appreciation over time. The left side of the figure shows how these three components contribute to your total return, while the right side displays how your Cash-on-Cash Return grows steadily, crossing the 5% benchmark within the first few years and continuing to increase substantially over the investment period.

This approach to wealth creation is what makes real estate particularly attractive as an investment vehicle, especially in markets with persistent housing shortages like the Netherlands.

Some Final Remarks

The analysis of the Maastricht property demonstrates that real estate investment is not a get-rich-quick scheme but a long-term wealth-building process requiring vision, hard work, and capital. The "blank canvas" of this house represents the reality that creating value in real estate demands significant effort and investment.

It's important to acknowledge that our exercise relies on many assumptions that may not reflect reality perfectly. Rental rates, renovation costs, and property appreciation could all vary significantly from our projections. The primary goal wasn't to provide a detailed analysis of this specific house, but to illustrate how to think about real estate investments systematically.

We've made specific choices in our model for clarity, a 30-year fixed-rate annuity mortgage at 4%, property appreciation at 3%, and rental increases at 2%. However, alternatives might prove more advantageous in practice. A linear mortgage would reduce total interest paid over time, and shorter fixed-interest periods might be preferable in today's declining interest rate environment.

The fundamental takeaway is that real estate wealth accumulates gradually through three mechanisms: regular cash flow, equity buildup, and property appreciation. When approached with realistic expectations and thorough analysis, investments like our Tongersestraat example can indeed deliver substantial returns, not overnight, but over decades.

Do you want a proper property analysis done? Do you want aid in the calculations of your real estate adventure? Reach out to me; contact@futurefunds.nl or send me a private message.