The Battle of Acquiring a Home

How will home prices develop in 2025?

Real estate represents one of the most significant investments many of us will ever make and continues to be a central topic in financial discussions worldwide. Are you currently renting? Have you recently purchased your first home? Or perhaps you're saving for a down payment while watching the market with concern? Understanding real estate trends is essential for making informed decisions, regardless of your current housing situation. The persistent housing shortage has become a defining political issue, with parties across the spectrum proposing various solutions to address the imbalance between supply and demand. How will decreasing interest rates and ongoing supply constraints affect your prospects? As a market that affects everyone and will remain relevant as long as humans need shelter, real estate deserves our thorough understanding. In this article, we'll explore the fundamental mechanics of the real estate market, examining the crucial role of mortgages and interest rates that underpin property values, alongside the current housing shortage. We'll approach this both from a personal perspective, helping homebuyers navigate their options, and from an investor's viewpoint, revealing opportunities to participate in real estate's growth. This dual perspective will provide you with the essential knowledge to navigate this market in 2025 and beyond.

Understanding debt, introducing mortgages

Let's first look at real estate on a personal level. If you want to buy a house, you probably do not have the money to just buy it outright. You will go to a bank and take out a mortgage to be able to buy the house. You will then proceed with paying off this mortgage over the number of years you choose, with 30 years being the most common term. As we know, borrowing costs money, and when borrowing is cheap, you are able to borrow more based on your income. You might already start seeing where I'm going with this, because what determines whether borrowing is expensive or cheap? Yes, interest rates. Therefore, understanding where interest rates go will theoretically show where housing demand will go.

Let me start with the basics of a mortgage. The most popular types are linear and annuity mortgages. Figure 1 perfectly shows how these two mortgages differ from each other. I have taken a €300,000 mortgage with the current interest rate for a 20-year fixed, 30-year term mortgage (which is quite common in the Netherlands) as an example to work with. The linear mortgage pays the same principal amount each period such that after 30 years you've paid off your mortgage. In the beginning, this means you pay a lot of interest as there is a lot of outstanding debt. The advantage of this mortgage is that each year you will pay less as the amount of outstanding debt decreases. With an annuity mortgage, you pay-off less money in the beginning and increase the principal gradually, resulting in the same monthly payment over the lifetime of the mortgage. A critical difference is the total amount of interest paid over the lifetime of the mortgage: with the linear mortgage this is €162,450 and with the annuity this is €191,017, a difference of 17.5%, quite a lot of money!

Figure 1

Tying mortgages to people's budget

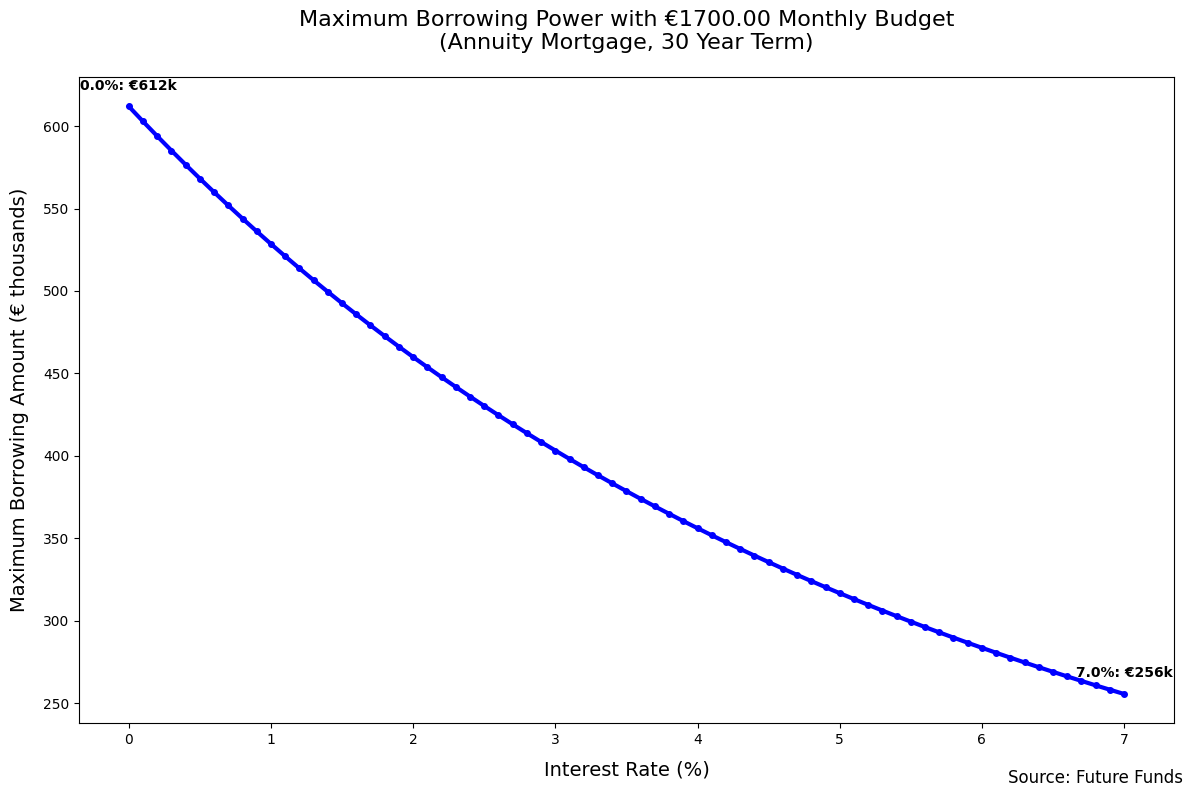

If we now think that this mortgage has to be paid with the salary of a household, we can start seeing the market dynamics of the housing market. Some numbers I found online stated that the average Dutch household earns around €75,000 a year, and that not more than 27% before tax should be spent on a mortgage (as an example, there is no “rule” for this). This means on a yearly level the household can spend around 21 thousand euros a year on a mortgage (around €1,700 a month).

With some reverse engineering that has been done in Figure 2, we can see that at the current 20-year fixed rate of 3.6%, this household would be able to borrow around €370,000. What this figure also shows is that this household will be able to borrow €400,000 when interest rates decrease further to 3%. This is because with lower interest rates, less of that €1,700 monthly payment goes toward interest, allowing more to go toward the principal loan amount.

The graph illustrates this inverse relationship clearly, as interest rates decline, borrowing power increases substantially. For instance, at 0% interest (though theoretical), a household could borrow over €612,000 with the same monthly budget. Conversely, if interest rates rose to 7%, the same household could only afford to borrow €256,000. This dramatic difference shows why interest rates are so crucial for housing affordability and, consequently, for housing prices.

Figure 2

The housing shortage

As already touched upon in the introduction, many countries are facing a severe housing shortage. In the Netherlands, this problem is particularly acute and is currently worsening each year. Figure 3 shows the projected growth of households that need housing (dark green bars) compared with the increment of new housing supply (light green bars). As you can see, the increment of households is currently larger than the increment of houses, meaning that each year the housing gap widens.

Figure 3 presents the official projection from the newly created Dutch ministry of housing, which is tasked with addressing this critical issue. If everything goes according to plan (which with governments is always tricky), we can only expect the housing shortage to stop worsening around 2027, when housing production finally catches up with household formation. Even more concerning, by 2039, they still project a cumulative shortage of around 218,000 homes (as indicated by the "Geschat tekort" notation)!

The orange dotted line tracks the total housing deficit over time, showing how it peaks before gradually declining, but never disappearing within this forecast period. This persistent imbalance means that on the supply side of the real estate market in the Netherlands, there simply isn't enough housing stock to meet demand, and this shortage will continue to be a significant factor in the market for the foreseeable future.

Figure 3

Outlook 2025 and beyond

As we explored at the beginning of this article, understanding real estate market dynamics is essential for making informed decisions, whether you're a potential homebuyer or an investor. We are currently in an interest rate lowering environment, and if the European Central Bank continues reducing its rates, which seems likely due to dampened inflation in Europe, this will eventually lead to lower mortgage interest rates. As we demonstrated in Figure 2, lower interest rates significantly increase borrowing capacity, allowing people with the same monthly budget to purchase more expensive properties, thus driving up housing demand.

When we combine this increasing demand with the severe supply constraints outlined in Figure 3, where the Dutch government projects housing shortages to persist well into the 2030s, the economic conclusion becomes clear. Basic economics tells us that when demand increases while supply remains constrained, prices rise. This fundamental imbalance creates a strong outlook for continued housing price appreciation in the coming years, particularly in markets like the Netherlands where the shortage is well-documented and severe.

Good one! It will be more and more difficult to own a home, when money is giving out by a state central institution

Great article! Thanks for sharing