Heijmans Delivers Exceptional 2024 Annual Results; Forecasts Strong Growth for 2025

Will this trend continue in 2025 and beyond?

It was not that long ago that Future Funds published its coverage of Heijmans stock. The journey started somewhere else, not with this stock, but with the question which stock performed the best in The Netherlands. This actually took a turn and made me dive into this company and discover that there is a reason for this incredible surge in the stock. On february 21st Heijmans published its annual report and the results are even better than most people would expect. Before reading this breakdown of their 2024 results and the outlook for 2025, I would highly recommend reading the piece on Heijmans here. Without further ado let's get into the report.

Key highlights and results

As talked about in the 2023 report, Heijmans aimed to increase its EBITDA margin to 7.5%. This number has actually been surpassed and they achieved an EBITDA margin of 7.7%.

A revenue of 2.5 billion was aimed for in the 2023 report, they delivered and ended up with a revenue of 2.584 billion.

The net result after tax in 2023 was 60 million, while delivering for the year 2024 a result of 90 million.

The yearly dividend Heijmans is doing this year will be 1.64 euro per share (a cash payout of 50%) compared to the dividend of 0.89 euro per share (a cash payout of 40%) that has been done in 2023.

The net debt of Heijmans has decreased to 10 million from the 134 million in 2023. They acquired this debt to be able to buy Van Wanrooij, which now is thus fully paid off.

Keeping a strong recurring revenue base with 40% of revenue being recurring in 2023 and 35% in 2024

Source, annual report Heijmans 2024

The management under the lead of Ton Hillen delivered on their promises and even exceeded in many of their promises. The margins and revenue have both substantially increased, the acquired debt because of the Van Wanrooij acquisition has already been paid off, while at first it was thought that this would be done by 2026. The acquisition of Van Wanrooij seems to be a smart decision as Heijmans has been able to increase their EBITDA margins significantly. The living segment of Heijmans where Van Wanrooij is operating has therefore also shown the biggest EBITDA margin increase from 7.1% in 2023 to 8.9% in 2024, with a revenue increase of 21% year over year. It is also seen that in this segment private buyers (+32%) are buying relatively more homes than housing corporations and investors (+13%).

The working segment of Heijmans has also delivered strong results with an EBITDA margin increase from 6.4% to 7.4% and an revenue increment of 18%. Heijmans states that they see a growing interest in this renovation segment of their business and added 2 large clients to their customer base: ASML and Royal Flora Holland.

Heijmans' connecting segment, which specializes in renovation and replacement of critical infrastructure, saw mixed results in 2024. While revenue grew significantly by 25%, the EBITDA margin decreased from 8.3% to 7.1%. However, this decline should be viewed in context, the 2023 margin was positively impacted by a one-time €14 million release of provisions in the Wintrack II project. Looking ahead, the segment's prospects appear strong, driven by the aging Dutch infrastructure, much of which was built in the post-World War II era and now requires substantial renovation.

Governance

The CEO Ton Hillen has demonstrated he is capable of delivering upon his promises and even doing a better job than how he personally forecasted the results. This is a good sign as it shows that we investors can put some trust in the management of Heijmans. Another notable decision by management to acquire Van Wanrooij has seemed to be a good decision of management, this acquisition allowed Heijmans to increase their revenue in the living sector and significantly increase EBITDA margin. Next to that it is noteworthy that the management is keen to pay off debt as fast as possible to ensure high solvency, the debt acquired to pay for the Van Wanrooij acquisition has been fully paid off, being a year earlier than the projected 2026. Next to that the management decided to celebrate this fantastic year along with the shareholders by increasing the dividend payout to 50% of cash, yielding shareholders a dividend of 1.64 euro.

Financials

Examining Heijmans' financial performance metrics reveals a compelling story of strategic growth and recovery. Figure 1 illustrates the company's Return on Equity (ROE) and Return on Invested Capital (ROIC) trends over the past three years, highlighting significant developments in capital efficiency.

The metrics experienced a notable decline in 2023, primarily due to the strategic acquisition of Van Wanrooij. ROE decreased from 22.4% to 21.1%, while ROIC saw a more pronounced drop from 33.3% to 11.4%. However, this temporary setback has proven to be a strategic investment, as evidenced by the robust recovery in 2024.

2024 marks a significant milestone, with ROE reaching an impressive 25.3%, the highest level in recent years. This exceptional return on equity, particularly noteworthy in the construction sector, demonstrates Heijmans' effective use of shareholder capital. The ROIC has also rebounded strongly to 19%, indicating that the company is efficiently converting its investments into profitable returns.

Figure 1

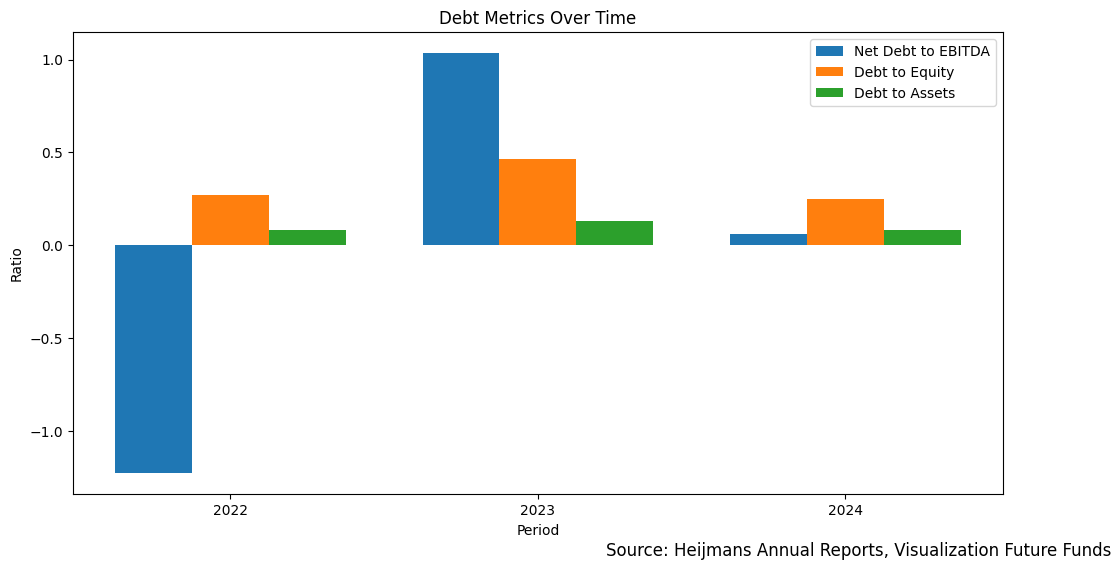

Heijmans' debt metrics continue to demonstrate strong financial discipline, as shown in Figure 2. While the Van Wanrooij acquisition temporarily increased Net Debt to EBITDA to 1.0x in 2023, the company swiftly reduced this to 0.1x in 2024. This conservative approach to debt management significantly minimizes default risk for shareholders.

Figure 2

Heijmans reached a remarkable Free Cash Flow of €251 million in 2024, primarily due to a €100 million reduction in working capital. Comparing valuations using Discounted Cash Flow analysis shows two different pictures: the 2023 analysis shows a company value of €900 million, matching current market value, while the 2024 analysis suggests a much higher value of €3 billion. While this jump is notable, it's important to understand that the exceptional €100 million working capital release won't repeat yearly and that this might skew the forecast.

The DCF analysis isn't meant to provide an exact company valuation but rather help us explore different future scenarios. Given the current market cap of €1 billion, the price-to-Free Cash Flow ratio of 25% is particularly attractive, as it indicates the company generates substantial cash flow relative to its market value. This robust cash generation capability, even accounting for the one-time working capital effect, suggests the company's fundamental value has strengthened and could support a higher valuation. High cash flow generation at this level provides the company with significant financial flexibility for future investments, debt reduction, or shareholder returns.

Figure 3, 900 million valuation

Figure 4, 3000 million valuation

Outlook for 2025

Heijmans is well-positioned for continued growth in 2025, driven by two key factors: the persistent Dutch housing shortage and the need for infrastructure renewal. Management under the lead of Ton Hillen has demonstrated strong execution, particularly with the successful Van Wanrooij acquisition. Their consistent focus on quality over quantity in project selection has driven superior financial results, setting them apart from competitors. Due to its robust financial position and proven management capabilities, demonstrated by a strong Return on Invested Capital (ROIC) of 19% and an impressive Return on Equity (ROE) of 25.3% - exceptional figures in the construction sector - Heijmans is likely to outperform its competition (Koninklijke BAM groep) in the sector. The company targets €2.75 billion in revenue with an 8% EBITDA margin in 2025. While this suggests more moderate growth compared to 2024, the fundamental drivers remain strong: deregulation efforts by the new ministry of living to increase housing supply, and the ECB's interest rate lowering which is beneficial for large-scale construction projects and housing demand. Despite the 14% post-earnings stock price increase, Heijmans' strong management track record and operational efficiency suggest continued growth potential ahead.